There is quite a strong demand among investors to use interest only loans to buy property in Australia. According to ASIC, the demand for interest only products has grown by about 80 per cent in the last three years.

Video: Investing in your Local Area

In this videeo, Robert Projeski, Managing Director for AMO, suggests how to structure a loan for your principal place of residents, and one for your investment property in order to maximise your tax deductions.

{youtube}ikKrZMCrFeQ{/youtube}

The Popularity of Interest Only Loans

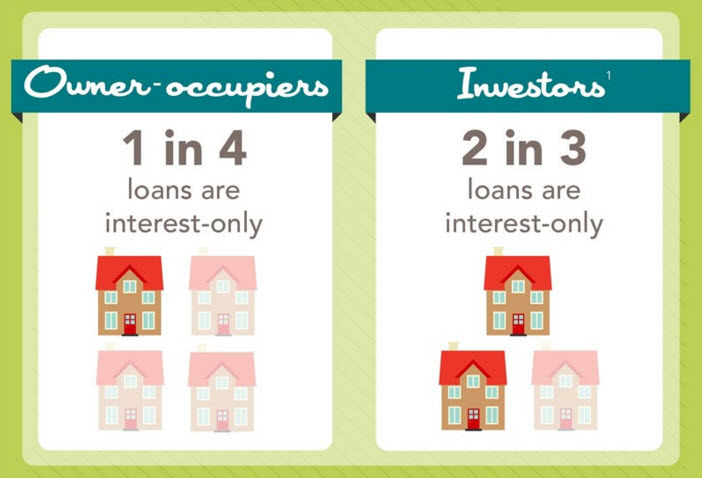

According to ASIC, interest only home loans had nearly doubled in Australia, jumping from $88.7 billion in 2012 to $142.8 billion in 2014 - two thirds of whom are property investors.

Source: ASIC The Average Interest Only Mortgage 2014

In a nutshell, an interest only loan is a loan whereby you only pay the portion of the interest on the loan. Most banks offer interest only loans for up to 5 years at a time, after which, your loan is reviewed to determine if you are able to continue to service the loan. After this period, you may apply for another 5 year extension to the loan, or switch to a different loan package.

Pitfalls of Interest Only Loans

The main disadvantage of a principal and interest loan is that the principal is not tax deductible. Therefore if you use a principal and interest loan, you will need to separate the deductions that you can claim.

If you plan to take out an interest only loan for your principal place of residence, you should be wary of paying too much interest over the life of the loan. Although you will pay more at the start, a principal and interest loan may work better for those that want to own their own home sooner. That's because paying down the principal will reduce the overall size of your mortgage, whereas paying the interest only component will not reduce your mortgage.

Advantages for Property Investors

Interest only loans are favoured by property investors as it allows them to accumulate more property, while using as little of their own money as possible.

Here are a few reasons for their popularity:

- Make Extra Repayments - one of the biggest mistakes by many first time investors is to think that they can only pay off the interest component on an interest only loan. As a result, they end up using a principal and interest loan to purchase their investment property. There are interests only loans that allows you to make extra repayments beyond the required minimum monthly repayments. As such you can reduce the size of your loan with an interest only loan by paying the principal component if you want to.

- Effective Use of After Tax Dollars - although many home buyers like the idea of a principal and interest loan, because it eventually reduces the size of their loan, it's also important to remember that you are effectively using after-tax dollars to pay down your loan. Therefore a $600 loan repayment may mean that you actually have to earn $700 before tax. As an investor, you are therefore better off using an interest only loan.

- Build up a Buffer - If you pay down the principal on your loan, you will eventually reduce the size of your loan. While it's always healthy to have a buffer in place in case of emergencies, reducing the size of your loan will eventually reduce your interest repayment, and thus the claim you can make on your tax deductions.

Building Wealth

If you do your due diligence and take out an interest only loan on your investment property, you will eventually reap the rewards of capital growth.

As an example, if you had purchased a unit in Bondi for $650,000 in 2013, your interest repayment at 5 per cent would be $2,708 per month. In 2016 the same property is now worth $917,500 - that's a gain of over $170,000 after you deduct all interest repayments. The loan and the interest repayment still remains, but at "yesterday's" rates, while the new capital growth and gains is at "today’s" rate.

Over time many property investors find that their negatively geared properties become positively geared. For example, the current median rent for units in Bondi is $2792 per month, effectively this is enough to cover the mortgage repayment of $2,708 per month on the unit.

Thus your aim in taking out an interest only loan is to leverage and build up equity. Your main aim here is to look for property that will experience strong capital growth, while using as little of your own money as possible.

AMO has a number of home loans that can help you to own your own home sooner or to leverage into buying an investment property. For example, our Prestige Home Loan comes with a 100 per cent offset account on either fixed or variable rate home loan, while our Construction Loan are ideal for those people wanting to make renovations to their home or investment property. For the perfect loan to suit your particular needs, book an appointment with our mortgage brokers or call us on 1300 266 266.